Every investor approaches their investment strategy a little bit differently. Some investors prefer to focus on high-growth companies, while others prefer the stability of more stable income-producing investments. But, one component that always seems to be evident inside investor portfolios is some variation of diversification.

Diversification is a nutshell is simply “spreading out your bets”. Instead of concentrating on a few individual investments, we make a number of investments to create a portfolio of some underlying assets. What that asset might be, depends on who the investor is.

For baby boomers, that breakdown might look more like a basket of dividend-paying stocks. Or, maybe a basket of stocks and bonds. For Gen Z, diversification might look like tech stocks, crypto, rare sneakers, and various NFTs.

However you define diversification is up to you, but the most important aspect is you are in fact diversified.

Too many investors over-concentrate their portfolios into a few single investments. Some investors have the entirety of their net worth tied up in their house. While others have all their life savings in their employer stock options. Whatever the scenario may be, the important part is to understand where the risk lies in your portfolio. Once you know where the risk lies in your portfolio, you can determine how best to diversify that risk away.

Now, this post is not geared to talk about diversifying your investment portfolio. We talk with investors every day on how to reduce risk and diversify out their investments. But when it comes to diversification, what else should you be thinking about? The answer…Tax Diversification.

Diversification is as important for your taxes as it is in your investment portfolio. Having a diversified tax base for your investments can significantly improve your after-tax returns. By effectively using tax-free, tax-deferred, and taxable investment vehicles, you can dramatically change the outcome of a financial plan.

Take Robinhood for example, one of the most highly valued, private technology companies. They currently manage over $80 billion in assets for more than 18 million customers. Yet, it only offers its clients taxable investment accounts. Plenty of investment choices to diversify but not much for diversifying your tax base.

Tax diversification is where I emphasize investors spend a little time. Most all of us spend the majority of our time focused on what investments should go into our account. The better question we should be evaluating is which account should our investments go into.

Compounding growth stocks in a Roth IRA will provide vastly different results when compared to a brokerage account. By simply eliminating the capital gains on the back-end of a stock sale, the net return to an investor is dramatically changed. Or, for municipal bonds paying tax-free interest, it makes a lot of sense in a brokerage account or trust while almost no sense in a retirement account. By understanding the tax diversification of our portfolio, we can better align our investments with our tax base.

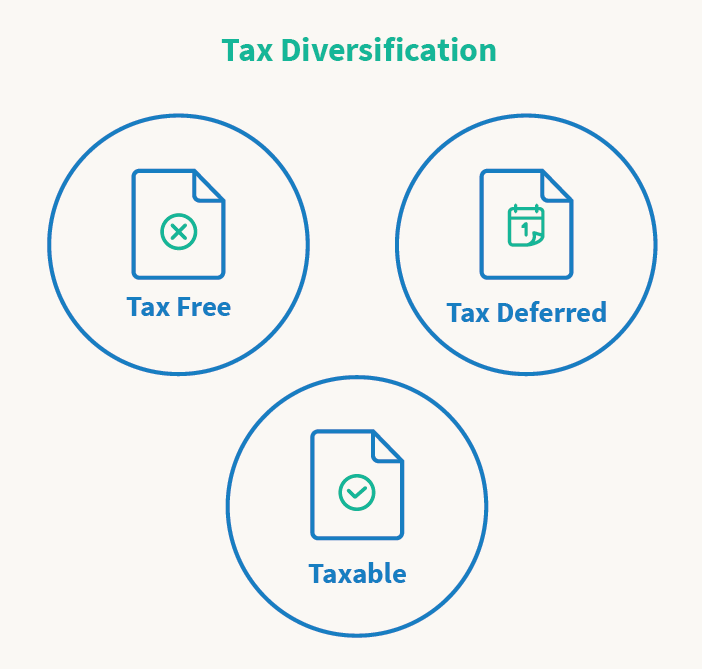

Below is a quick summary of the different accounts in each bucket. This list isn’t entirely complete but more of a high-level overview of options in each category.

Tax-Free:

- Roth IRA

- HSA for health expenses

- Life Insurance Cash Value

Taxable:

- Brokerage Accounts

- Trust Accounts

- Business Accounts

Tax-deferred:

- Traditional IRA

- 401k or 403b

- Pension Plan

- Annuities

The most important aspect is to understand your tax situation and the tax rules associated with each account. If you are not sure where to go, that’s where an advisor can help!

Disclosure:

Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, asset class, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. Past performance is not indicative of future performance.

This article should not be considered an endorsement of any platforms, websites, or products discussed. All information provided is the opinion of the author and does not directly represent the views of Csenge Advisory Group.