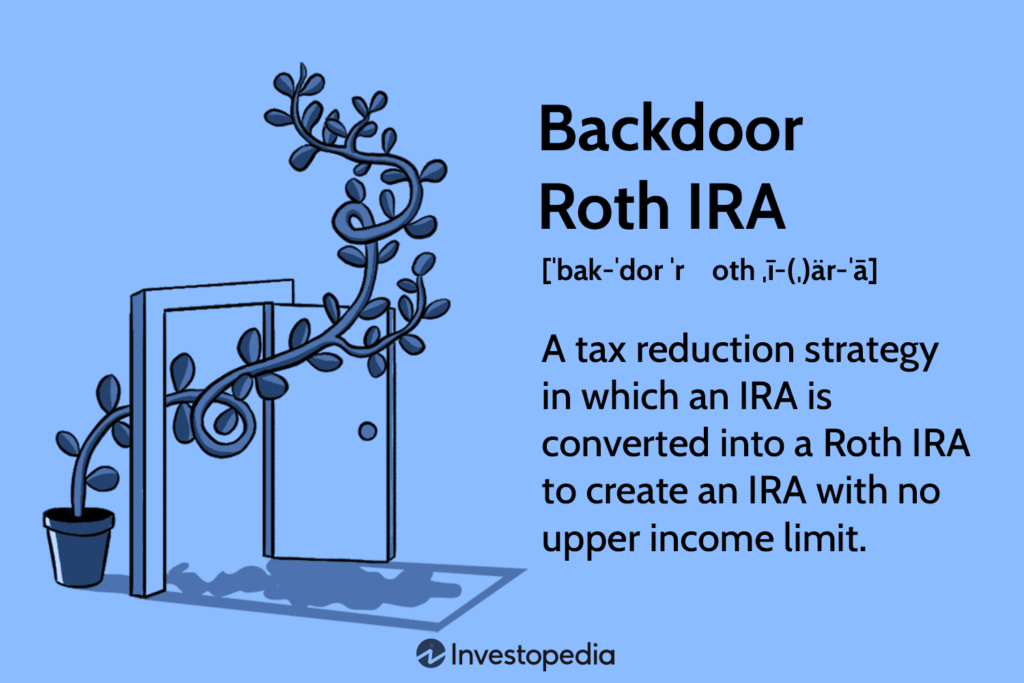

A backdoor Roth contribution is a way for individuals to contribute to a Roth individual retirement account (IRA) even if they exceed the income limits for traditional Roth contributions. This strategy involves making a nondeductible contribution to a traditional IRA and then converting the balance to a Roth IRA.

Here’s how it works:

- Make a non-deductible contribution to a traditional IRA. This type of contribution can be made by anyone, regardless of income level.

- Convert the balance of the traditional IRA to a Roth IRA. This is known as a “backdoor Roth contribution.”

It’s important to note that while the backdoor Roth contribution strategy can be a useful way for high earners to save for retirement, it is not without its risks. For example, the IRS has the right to disallow the conversion if it determines that the conversion was not a “bona fide” conversion and was instead intended to evade the income limits for traditional Roth contributions.

If you have questions about a backdoor Roth contribution or your personal retirement accounts, please reach out to one of our advisors! It’s always a good idea to consult with a financial advisor or tax professional before implementing this or any other retirement savings strategy.